Losses and damages of weather-related disasters are increasing

In the face of climate change, BoP communities in many developing countries are becoming increasingly vulnerable to the risks posed by extreme weather and climatic events. Climate change-related impacts affect agricultural productivity, weaken water and food security, increase the incidences of diseases, and threaten existing basic infrastructure. The Munich Re estimates that the average annual weather-related disaster costs in the past five to ten years in “low” and “lower middle income” economies have reached an upward price tag of US$ 1.3 billion and US$ 6.8 billion respectively.

In particular, the agricultural sector is heavily impacted by unpredictable rain patterns and long periods of drought. The adverse effects of climate change disproportionally affect agricultural smallholders as their capacity to manage climate change-related risks is limited by various constraints such as the lack of reliable irrigation and affordable high-quality agricultural inputs such as seeds and fertilizer. In addition, their increased risk-exposure curbs agricultural investment – a key vehicle in improving smallholders’ livelihoods.

Climate risk insurance increases the adaptive capacity of smallholders

How can climate risk insurance help smallholders? Let’s think, for a moment, about a maize farmer in Rwanda. Like 80% of his fellow countrymen, his livelihood is heavily dependent on agricultural production but he only possesses a piece of land that is 0.59 ha – barely sufficient for subsistence farming. He does not use any fertilizer nor improved seeds to increase his yields  and has very little material savings to invest in adaptation measures. As such, his entire yield and few material savings can be wiped out in a single bad harvest. If such an unfortunate event occurs, he will have very little to provide his family with—and since his neighbors are also likely to be equally exposed to the natural hazard—there is no one in his community he can borrow from.

and has very little material savings to invest in adaptation measures. As such, his entire yield and few material savings can be wiped out in a single bad harvest. If such an unfortunate event occurs, he will have very little to provide his family with—and since his neighbors are also likely to be equally exposed to the natural hazard—there is no one in his community he can borrow from.

For the Rwandan maize farmer and others like him, climate risk insurance can provide security against climate-related yield, livestock, dwelling and livelihood losses. Even loss of lives in the post-disaster period may be covered by climate risk insurance. In a worst-case scenario of a climate-related disaster, the maize farmer will receive the money needed to support his family and get back on his feet again after the event. With this safety net in mind, he will have more confidence investing in his and his family’s future.

Insurance models reduce smallholders’ sensitivity and exposure against climate related risks

In addition helping farmers to cope with the shock after a disaster, innovative insurance mechanisms can support farmers to invest in risk prevention and reduction measures that will help them to reduce their sensitivity against climate related risks. In a recent study, Endeva identified four main insurance models that increase smallholders’ resilience by:

(1) rewarding risk reducing behaviour (e.g. through smaller premium payments);

(2) actively paying smallholders to implement disaster risk reduction (DRR) measures;

(3) informing about approaching weather events; and

(4) paying out in anticipation of the occurrence of the event to allow farmers to better protect themselves against the natural hazard.

The Market of Climate Risk Insurance

Today, climate risk insurance is not widely available for the BoP in developing countries. In 2011, only 6.5% of people working in agriculture in Sub-Saharan Africa and 5.7% in South Asia purchased insurance against climate-related risk. This correlates to approximately 55 million people living on less than US$ 2 a day in Africa, Asia and Latin America that are covered by direct insurance schemes against climate risks.

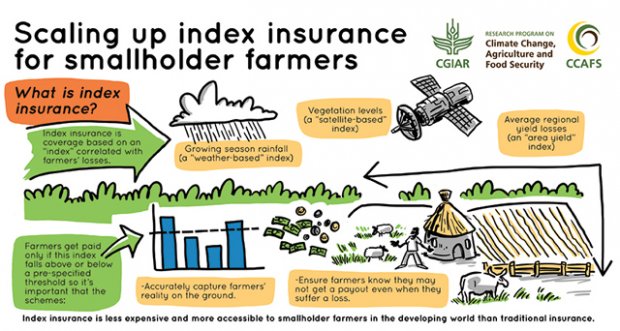

The most frequent type of climate risk insurance is an index-based insurance model. Index-based means that farmers do not get paid for their losses on individual case level but based on objectively verifiable data of an observed weather event (see map). These insurance models are less costly for farmers because the insurer doesn’t have to assess the loss and damage for every single case, reducing the administration costs. But farmers also face a risk of incurring a loss without receiving a payout.

Source: CCAFS and CGIAR

Source: CCAFS and CGIAR

Given that today an estimated 1.5 billion people directly depend on agriculture for their income, the potential market for climate risk insurance, especially agricultural micro-insurance, poses a significant financial opportunity. In fact, different models are currently being tested in a wide variety of settings to support smallholder farmers in coping with the effects of climate change such as droughts, floods, or increased frequency and severity of infestations.

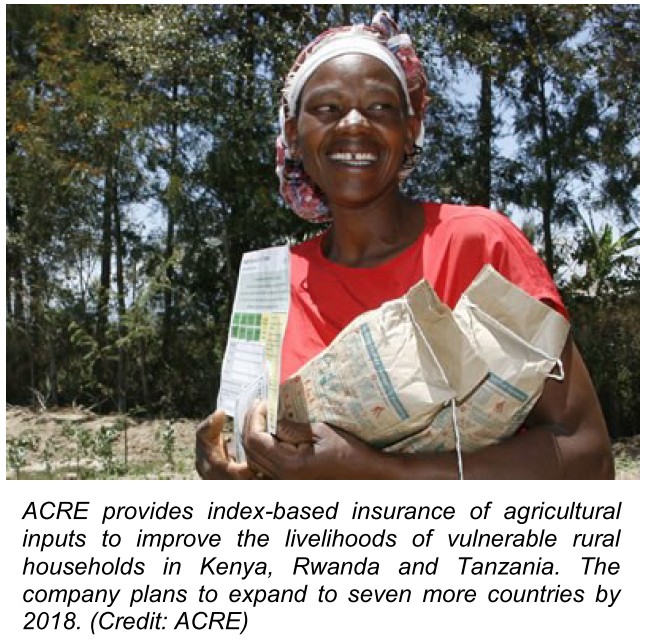

ACRE makes crop insurance affordable for the BoP

The insurance company UAP in Kenya developed the insurance product “Kilimo Salama” that requires smallholders to implement DRR measures to be granted access to insurance coverage. In partnership with the Syngenta Foundation for  Sustainable Agriculture and the telecoms operator Safaricom, UAP designed Kilimo Salama in 2009 based on a pilot where several hundred maize farmers insured their farm inputs against droughts and torrential rainfalls.

Sustainable Agriculture and the telecoms operator Safaricom, UAP designed Kilimo Salama in 2009 based on a pilot where several hundred maize farmers insured their farm inputs against droughts and torrential rainfalls.

Since 2014, Kilimo Salama has developed into the Agriculture and Climate Risk Enterprise (ACRE), the largest agricultural insurance program in Sub-Saharan Africa with 285,000 policies sold in the East African countries of Kenya, Tanzania and Rwanda. By 2018, they intend to provide insurance for three million farmers in ten countries.

The use of mobile technology is a key success factor of this model’s ability to reach smallholder farmers. Through a collaboration with M-PESA’s mobile banking scheme, clients can easily pay premiums and receive payouts, lowering the transaction and delivery costs of the insurance product.

ACRE offers its customers a replanting guarantee. In collaboration with seed companies the insurance premium is incorporated into the price of every bag of seeds. Each bag contains a scratch card with a code inside. To register for the insurance, farmers message the code to ACRE via SMS. The replanting guarantee starts upon registration and ends after two weeks. If there is a drought or excessive rainfall within that period, smallholders receive a voucher for a new bag of seeds. This enables them to replant again within the same season. Insuring inputs (e.g. seeds) rather than outputs (yields) significantly reduces the price of their insurance premium and makes the product even affordable for farmers with very little additional income.

ACRE insurance pays for smallholders. An impact study conducted in 2012 found that insured farmers invest 19% more than their uninsured peers. In addition, their income is 16% higher and 97% of insured farmers receive loans that were linked to insurance. Most of these farmers would not have been eligible for credit otherwise.

Other innovative insurance models follow

Other innovative insurance models include the Rural Resilience Initiative – Harita (R4) in Ethiopia and the Indian insurer People Mutuals. R4 accepts labour contribution into disaster risk reduction and adaptation measures in exchange for the premium payment. This makes its insurance accessible to even the poorest smallholders. People Mutuals provides smallholders with the required goods and services, e.g. by providing training and information on water management or good agricultural practices.

The way forward

This blog series demonstrated that companies from different sectors can engage in market-based solutions that increase the climate resilience of BoP communities. With COP 21, there exists a new momentum for climate change that should be used to bring the business community and the development community closer together and develop adaptation approaches for a world where we and future generations want to live in. I hope this blog series will inspire some further research, thinking and discussion in that direction!

This blog was authored by Christian Pirzer and is part of the Practitioner Hub’s series on climate change and inclusive business.

{kind=link}